Introduction: Why Clean Books Are Your Best Business Asset

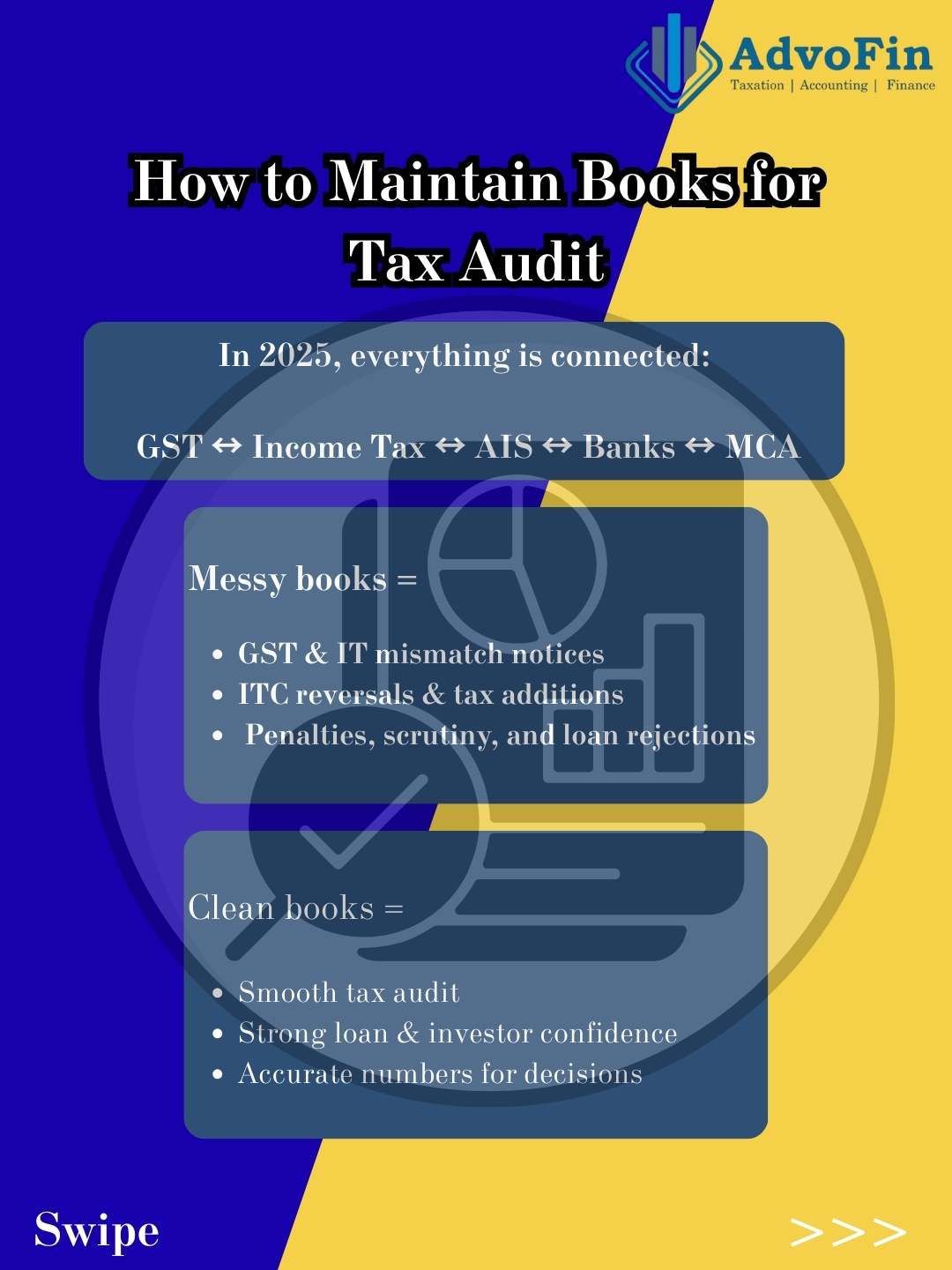

In 2025, Indian compliance has become ruthlessly integrated. Your GST data talks to your Income Tax records. Your bank transactions feed into AIS. Your TDS filings cross-verify with your books. Your MCA filings must match your financials.

Poorly maintained books of accounts now trigger:

❌ Automatic mismatch notices from GST and Income Tax

❌ Expense disallowances costing lakhs in additional tax

❌ Increased scrutiny and audit probability

❌ ITC reversals blocking working capital

❌ Penalties up to ₹1,50,000 for audit non-compliance

❌ Loan rejections and investor concerns

❌ Wrong financial decisions based on inaccurate data

Whether you’re a bootstrapped startup, growing SME, or established mid-market company, maintaining professional books is no longer optional – it’s survival.

If you’re subject to Tax Audit under Section 44AB (which applies to most businesses with turnover above ₹1 crore or professionals above ₹50 lakh), your books must meet specific statutory standards.

This guide gives you a complete, founder-friendly, legally compliant system to maintain books that will pass:

- Tax Audit under Section 44AB

- GST audits and assessments

- Bank and investor due diligence

- MCA scrutiny for ROC filings

Let’s build this system step by step.

Who Legally Must Maintain Books of Accounts?

Under Income Tax Act (Section 44AA):

You MUST maintain books if:

| Category | Threshold |

| Business (trading/manufacturing) | Turnover > ₹10 lakh OR Total income > ₹2.5 lakh |

| Professional (consultants, doctors, lawyers, etc.) | Gross receipts > ₹25 lakh OR Total income > ₹2.5 lakh |

| Subject to Tax Audit (Section 44AB) | Business > ₹1 crore turnover OR Professional > ₹50 lakh receipts |

| Not opting for presumptive scheme | Any business not under 44AD/44ADA/44AE |

Under GST Act:

Every registered person must maintain proper accounts including:

- Sales register (outward supplies)

- Purchase register (inward supplies)

- Input tax credit records

- Stock records (opening, receipt, dispatch, closing)

- Payment and collection records

- E-way bill documentation

Bottom Line: If you’re doing business in India and crossing even basic thresholds, maintaining books is mandatory – not optional.

The Complete List of Books Required for Tax Audit (2025)

To pass tax audit without qualifications or penalties, you need three categories of records:

A) Primary Books (The Foundation)

1. Sales Register/Revenue Register

- Date-wise sales entries

- Customer name and GSTIN (if registered)

- Invoice number and date

- Taxable value and GST

- Payment terms and collection status

2. Purchase Register

- Date-wise purchase entries

- Vendor name and GSTIN

- Bill number and date

- Taxable value and ITC eligible/ineligible

- Payment status

3. Cash Book

- All cash receipts and payments

- Opening and closing balance daily

- Must match physical cash count

4. Bank Book (for each bank account)

- Every bank transaction recorded

- Regular reconciliation with statements

- Separate books for each account

5. General Ledger

- All accounts maintained (assets, liabilities, income, expenses)

- Party-wise ledgers (debtors/creditors)

- Expense head-wise ledgers

- Opening and closing balances

6. Journal Entries Register

- All non-cash transactions

- Adjusting entries

- Accruals and provisions

- Proper narration for each entry

7. Fixed Asset Register

- Asset-wise details (date of purchase, cost, depreciation rate)

- Additions and deletions during the year

- WDV calculation

- Physical location and condition

B) Statutory/Compliance Registers

1. GST Output Register

- Summary of GSTR-1 filed

- Month-wise taxable sales

- GST liability

2. GST Input Register (ITC Register)

- Based on GSTR-2B (not 2A)

- Eligible vs blocked ITC

- ITC reversal tracking

- Vendor compliance status

3. RCM (Reverse Charge) Register

- Expenses under RCM

- RCM liability calculated and paid

- ITC claimed on RCM

4. TDS Register

- Party-wise TDS deduction

- Challan details (BSR, date, amount)

- Quarterly return filing status

- Certificates issued

5. E-Way Bill Register

- Transport-wise records

- Invoice matching

- Vehicle details

- Validity tracking

6. Stock/Inventory Register

- Opening stock

- Purchases/production

- Sales/consumption

- Closing stock

- Valuation method (FIFO/Weighted Average)

C) Supporting Documents (Audit Defense File)

Must maintain in organized manner:

- All original invoices (sales and purchases)

- Expense bills with proper supporting

- Debit and credit notes

- Bank statements and reconciliation working

- Payment vouchers and receipts

- Contracts and agreements (vendors, customers, employees)

- Party confirmation letters (debtor/creditor balances)

- Loan agreements and sanction letters

- Capital contribution documents

- Board resolutions (for companies)

- Partnership deed (for partnerships)

Storage Duration: Minimum 7 years (8 years recommended)

Choosing Your Accounting Method (Critical Decision)

1. Accrual Method (Recommended for Most Businesses)

How it works:

- Revenue recorded when earned (invoice raised), not when cash received

- Expense recorded when incurred (bill received), not when paid

- Gives true picture of business performance

Who should use:

- All Private Limited Companies (mandatory)

- All LLPs (mandatory)

- Partnerships and proprietorships with turnover > ₹50 lakh

- Any business planning to raise funding

- Businesses with credit sales/purchases

Example: Invoice raised in March, payment received in April → Revenue recorded in March

2. Cash Method

How it works:

- Revenue recorded only when cash received

- Expense recorded only when cash paid

- Simpler but doesn’t reflect true financial position

Who can use:

- Very small proprietorships

- Professionals under presumptive taxation (44ADA)

- Businesses with mostly cash transactions

Critical Mistake Founders Make:

Running a business with ₹1-2 crore turnover, multiple employees, credit sales, and inventory – but maintaining books on cash basis like a small shop.

Result: Financial statements don’t reflect reality, investors reject you, banks won’t lend, and auditors qualify the report.

Rule of Thumb: If your turnover exceeds ₹50 lakh or you have inventory, use accrual method.

The Founder’s Bookkeeping System (Daily/Weekly/Monthly)

Professional books aren’t built at year-end – they’re built with daily discipline.

Daily Tasks (15-30 minutes)

What to do:

- Record all expenses paid (even petty cash)

- Upload bills/invoices to shared folder immediately

- Record all sales invoices generated

- Track payments received from customers

- Update payment reminders for overdue invoices

- Verify cash in hand matches cash book

Tools:

- Google Drive folder: “Daily Invoices → [Month] → [Date]”

- WhatsApp group with accountant for instant document sharing

- Digital payment screenshots saved immediately

Why daily matters: One missed invoice today becomes 10 missed invoices by month-end, creating chaos during GST filing.

Weekly Tasks (1-2 hours)

What to do:

- Bank reconciliation for all accounts

- Cash book balance verification

- Review vendor outstanding (who to pay this week)

- Review debtor outstanding (who to follow up with)

- Payroll data collection (attendance, overtime, deductions)

- Verify all documents uploaded properly

Weekly Review Meeting: 15-minute call with your accountant covering:

- This week’s revenue

- Major expenses

- Outstanding collections

- Payments to be made

- Any issues or missing documents

Monthly Tasks (MOST CRITICAL – 3-5 hours)

This is where tax audit readiness is built:

1. GST Reconciliation (Top Priority):

- Sales register matches GSTR-1 outward supplies

- Purchase register matches GSTR-2B (not 2A)

- ITC claimed only for eligible items in 2B

- Credit/debit notes properly recorded

- Export and exempt supplies correctly classified

2. Financial Reconciliation:

- Bank reconciliation completed (zero unreconciled items)

- Cash book balanced

- Party ledgers reconciled (confirm balances with major vendors/customers)

- Loan EMI entries posted correctly (principal + interest split)

- Capital account updated

3. Expense Review:

- All expenses properly classified (not dumped in “misc expense”)

- Personal expenses removed from books

- Capital vs revenue expenditure correctly classified

- Blocked ITC items (personal use, motor vehicles, etc.) identified

4. Statutory Compliance:

- TDS deducted and deposited

- GST liability paid

- PF/ESI paid if applicable

- Professional tax paid

5. Asset & Inventory:

- Fixed asset register updated (new purchases, disposals)

- Depreciation schedule maintained

- Stock register updated

- Physical vs book stock variance investigated

6. Journal Entries:

- Accruals posted (expenses incurred but not billed)

- Prepayments adjusted (advance paid, expense in next month)

- Provisions created (audit fees, bonus, etc.)

The Golden Rule: Close each month’s books by the 10th of the next month as if it’s year-end. This makes actual year-end a breeze.

Choosing the Right Accounting Software

For Turnover < ₹1 Crore:

Option 1: Zoho Books

- Cloud-based

- GST-compliant

- Mobile app available

- Pricing: ₹1,500-2,500/month

Option 2: Vyapar

- Simple, India-focused

- Good for basic invoicing + GST

- Affordable: ₹4,000-8,000/year

Option 3: QuickBooks

- If dealing with international clients

- Multi-currency support

- Pricing: ₹1,800-3,000/month

For Turnover > ₹1 Crore:

Option 1: Tally Prime (Gold Standard)

- Most widely used in India

- Robust and reliable

- Auditor-friendly

- On-premise or cloud

- License: ₹54,000/year (multi-user)

Option 2: Busy Accounting

- Excellent for traders and manufacturers

- Strong inventory management

- Pricing: ₹25,000-60,000/year

Option 3: Zoho Books Enterprise

- For tech/SaaS startups

- Integrates with Zoho CRM, Projects

- Subscription-based pricing

For Startups with Subscription Business:

Option 1: Zoho Books + Chargebee

- Handles recurring billing

- Auto-invoicing

- Payment gateway integration

Option 2: Razorpay X Books

- Integrated with payment collection

- Auto bank reconciliation

- Good for digital businesses

Critical Advice: Never rely only on Excel sheets for maintaining books if your turnover exceeds ₹25 lakh. Tax auditors can reject Excel-based books as “not proper books of accounts.”

Ensuring Perfect GST-Books Synchronization (Most Common Audit Issue)

This is where 60% of tax audit qualifications happen. Here’s how to avoid them:

1. Books vs GSTR-1 Reconciliation

Monthly check:

| Item | Books | GSTR-1 | Match? |

| Total B2B Sales | ₹45,00,000 | ₹45,00,000 | ✓ |

| Total B2C Sales | ₹12,00,000 | ₹12,00,000 | ✓ |

| Export Sales | ₹8,00,000 | ₹8,00,000 | ✓ |

| Credit Notes | ₹2,00,000 | ₹2,00,000 | ✓ |

Common mismatches:

- Invoice entered in wrong month in GSTR-1

- Duplicate invoice entries

- Sales shown in books but not filed in GSTR-1

- Different values (₹1,00,000 in books vs ₹1,10,000 in GSTR-1)

Fix immediately: Any mismatch should be corrected in the same month using debit/credit notes or amended GSTR-1.

2. Books vs GSTR-3B Reconciliation

Check every month:

| Item | Books | GSTR-3B | Match? |

| Output tax liability | ₹8,10,000 | ₹8,10,000 | ✓ |

| ITC claimed | ₹5,60,000 | ₹5,60,000 | ✓ |

| Tax paid in cash | ₹2,50,000 | ₹2,50,000 | ✓ |

| Interest paid | ₹5,000 | ₹5,000 | ✓ |

3. Books vs GSTR-2B Reconciliation (CRITICAL)

This determines your ITC eligibility:

Process:

- Download GSTR-2B on 14th of next month

- Match with your purchase register

- Create ITC reconciliation:

| Vendor | Amount in Books | Amount in 2B | ITC Eligible | ITC Blocked | Reason for Block |

| Vendor A | ₹1,00,000 | ₹1,00,000 | ₹18,000 | – | – |

| Vendor B | ₹50,000 | – | – | – | Vendor not filed |

| Vendor C | ₹30,000 | ₹30,000 | – | ₹5,400 | Motor vehicle |

- Claim only ITC shown in 2B

- Track blocked ITC separately for future claim when vendor files

Why this matters: Claiming ITC not in 2B = automatic notice + 18% interest + reversal demand.

4. Books vs E-Way Bill Reconciliation

For businesses moving goods:

Match:

- Quantity in invoice = Quantity in e-way bill

- Value in invoice = Value in e-way bill

- Vehicle numbers accurate

- No expired e-way bills

Audit tip: Print e-way bill register and attach to invoice file for physical verification.

Founder Controls You MUST Implement (Non-Negotiable)

If you want trouble-free tax audit, these controls are mandatory:

Control 1: Set Monthly Closing Date

Example: “All books must be closed by 7th of next month.”

After this date:

- No backdated entries allowed

- Any corrections go through journal entries

- Prior month is “locked” in software

Benefit: Forces discipline, prevents manipulation, creates audit trail.

Control 2: Document Sharing SOP (Standard Operating Procedure)

Rule: Every invoice/bill must be shared within 24 hours of transaction.

Method:

- Vendor invoices: WhatsApp to accountant immediately

- Expense bills: Photo + upload to Google Drive daily

- Sales invoices: Auto-generated and saved in system

- Bank transactions: Connect bank feed to accounting software

Consequence for non-compliance: Transaction won’t be booked if document missing.

Control 3: Ledger Group Discipline (Prevent Misposting)

Create clear expense categories:

Operating Expenses:

- Employee salaries

- Office rent

- Electricity and utilities

- Internet and telecom

- Travel and conveyance

- Marketing and advertising

- Professional fees

Financial Expenses:

- Bank charges

- Interest on loans

- Processing fees

Capital Expenditure:

- Furniture and fixtures

- Computer and software

- Plant and machinery

- Vehicles

Personal/Non-Deductible:

- Personal drawings

- Penalties and fines

- Personal life insurance

- Family expenses

Never use: “Miscellaneous Expenses” as a dumping ground. Each expense must have proper head.

Control 4: Maker-Checker System

Two-person review process:

Maker (Accountant):

- Enters all transactions

- Prepares monthly reports

- Does reconciliations

Checker (Senior Accountant/CA/Advisor):

- Reviews all entries monthly

- Verifies reconciliations

- Signs off on monthly close

Benefit: Catches errors before they compound, ensures second set of eyes on everything.

Control 5: Year-End Controls (April-May)

Before closing books for FY:

Physical Verification:

- Stock count (physical vs books)

- Fixed asset verification (assets exist physically)

- Cash count (matches cash book)

Reconciliations:

- All bank accounts reconciled (zero pending items)

- All party ledgers reconciled (get written confirmations)

- Loan accounts reconciled with bank/lender statements

- TDS reconciliation (Form 26AS matches books)

Documentation:

- All invoices filed properly

- All agreements compiled

- All statutory payment receipts organized

- Board resolutions/partnership decisions documented

Common Mistakes SMEs Make (Tax Audit Red Flags)

❌ Mistake 1: No Backup of Invoices

What happens:

- Hard drive crashes

- Files lost

- Can’t produce invoices during audit

Solution:

- Cloud backup mandatory (Google Drive, Dropbox)

- Physical file for major invoices

- Daily backup routine

❌ Mistake 2: Personal Expenses Booked as Business

Examples:

- Family vacation as “business travel”

- Personal car expenses (when not used for business)

- Home renovation as “office renovation”

- Children’s school fees as “professional development”

Consequence:

- Expense disallowed

- Additional tax + interest

- Penalty possible

Solution: Keep personal and business 100% separate. If mixed use (like home office), claim only proportionate business use with documentation.

❌ Mistake 3: GST Mismatch (Biggest Risk)

Common gaps:

- Turnover in GST ₹80 lakh, in ITR ₹60 lakh

- ITC claimed ₹5 lakh in GST, expenses shown ₹3 lakh in ITR

- Sales recorded in different periods

Consequence:

- Both GST and Income Tax notices

- Demand from both departments

- Penalty and interest

Solution: Monthly GST-books reconciliation (not yearly).

❌ Mistake 4: Unexplained Cash Deposits

Scenario: ₹15 lakh cash deposited in bank, but income shown only ₹8 lakh.

Department asks: Where did ₹15 lakh come from?

Solution:

- Minimize cash deposits

- If unavoidable, maintain source documentation

- Sale of assets, loans, withdrawals from another account – all must be documented

❌ Mistake 5: Missing Vendor Invoices

Scenario: Claimed ₹10 lakh expenses, but bills available only for ₹7 lakh.

Result: ₹3 lakh expense disallowed = ₹90,000 additional tax (at 30%).

Solution:

- Never pay vendor without taking invoice

- Maintain vendor invoice file

- Follow up immediately for missing bills

❌ Mistake 6: Wrong Expense Classification

Example: Bought computer for ₹80,000 → Shown as expense.

Correct treatment: Capital asset (depreciation over years, not immediate expense)

Another example: Building repair ₹2,00,000 → Shown as repair expense Actually: Major renovation (capital expenditure)

Solution: Understand difference between revenue and capital expenditure. When in doubt, ask your CA.

❌ Mistake 7: Taking ITC on Blocked Items

Common blocked items:

- Personal motor vehicles

- Food and beverages for employees

- Health insurance (personal)

- Club membership

- Guest house maintenance

Result: ITC reversal + interest + penalty

Solution: Review Section 17(5) of GST Act and mark all blocked items separately at time of purchase.

❌ Mistake 8: TDS Not Deducted or Deposited Correctly

Impact:

- Expense disallowed under Section 40(a)(ia)

- Interest and penalty

- Vendor relationship damaged (they don’t get TDS credit)

Solution:

- Maintain monthly TDS register

- Deduct at correct rate at time of booking (not payment)

- Deposit by 7th of next month

- File quarterly returns on time

❌ Mistake 9: Stock Records Mismatch

Scenario: Opening stock: ₹10 lakh

Purchases: ₹50 lakh

Sales: ₹45 lakh

Closing stock (physical): ₹12 lakh

Calculation: ₹10L + ₹50L – ₹12L = ₹48L (cost of goods sold) But sales were only ₹45L → Operating at loss?

Mismatch indicates:

- Stock theft/damage not recorded

- Sales not recorded (cash sales hidden)

- Wrong valuation

Solution:

- Monthly stock reconciliation

- Physical verification quarterly

- Investigate and document variances immediately

Your Tax Audit Preparation Checklist

30 days before audit, ensure:

Books Finalization:

- All transactions recorded (no pending entries)

- Books closed and locked for the year

- Software backup taken

- No post-year-end adjustments needed

Reconciliations:

- Bank reconciliation (all accounts, zero pending)

- Cash book balanced

- GST reconciliation (GSTR-1, 3B, 2B vs books)

- TDS reconciliation (26AS vs books)

- Loan reconciliation (with statements)

- Party confirmations obtained (major debtors/creditors)

Financial Statements:

- Draft Profit & Loss prepared

- Draft Balance Sheet prepared

- Schedules and notes to accounts prepared

- Prior year comparative included

Statutory Registers:

- Fixed asset register updated and printed

- Stock register updated and valued

- GST registers compiled

- TDS register compiled

- E-way bill register ready

Documentation:

- All invoices filed chronologically

- Expense bills organized

- Contracts and agreements compiled

- Board resolutions/partnership decisions filed

- Statutory payment receipts organized

- Bank statements and reconciliation working filed

Compliance Proof:

- All GST returns filed (check on portal)

- All TDS returns filed (24Q, 26Q)

- PF/ESI challans available

- Professional tax paid

- ROC filings done (if company/LLP)

Management Representations:

- No contingent liabilities disclosure prepared

- Related party transactions listed

- Events after balance sheet date documented

- Management letter drafted (explaining any unusual items)

Audit Queries Anticipation:

- List of expected questions prepared

- Supporting evidence ready for:

- Large one-time expenses

- Capital expenditure

- Loans taken/given

- Sudden revenue/expense changes

A well-prepared file means:

- Audit completes in 3-5 days (not weeks)

- Minimal queries

- No qualification in audit report

- Clean certificate issued

Key Takeaways

Maintaining books for tax audit isn’t about perfect accounting – it’s about discipline, documentation, and monthly hygiene.

The businesses that pass audits smoothly:

✅ Maintain books monthly (not yearly)

✅ Reconcile everything (GST, TDS, bank, parties)

✅ Keep all documents organized and backed up

✅ Separate personal and business completely

✅ Use proper accounting software

✅ Review financials quarterly

✅ Implement maker-checker controls

✅ Close books by 10th of next month

The businesses that face audit nightmares:

❌ Do bookkeeping only at year-end

❌ Mix personal and business

❌ Lose documents and invoices

❌ Never reconcile GST with books

❌ Use Excel-only or no software

❌ Make backdated entries freely

❌ Ignore monthly discipline

The Choice Is Yours.

Clean books are not an expense – they’re an asset that:

- Prevents notices and scrutiny

- Secures loans and funding

- Saves taxes through proper planning

- Gives you accurate business intelligence

- Creates peace of mind

Build the system now, and tax audit becomes a formality – not a nightmare.

Frequently Asked Questions (FAQs)

Q1: Can I maintain books in Excel or do I need accounting software?

For very small businesses (turnover < ₹10 lakh), Excel may be acceptable, but it has serious limitations. For anything larger, use proper accounting software. Tax auditors can reject Excel-based records as “not constituting proper books” under Section 44AA, especially if they lack audit trails, are not backed up, or allow easy manipulation.

Q2: How long must I keep my books and supporting documents?

Minimum 7 years from the end of the relevant assessment year. For example, for FY 2024-25 (AY 2025-26), keep records until at least March 2033. However, 8 years is safer as the department can reopen assessments up to 10 years in certain cases (foreign assets, serious evasion).

Q3: What’s the penalty for not maintaining books when required?

Under Section 271A:

- Penalty of ₹25,000 if you fail to keep books when required

- Under Section 271B: Penalty of ₹25,000 to ₹1,50,000 if you fail to get accounts audited when required

- Plus interest on any additional tax demand arising from lack of proper books

Q4: Can I switch from cash to accrual method (or vice versa) mid-year?

Generally no. You should use a consistent accounting method throughout the year. If you want to change methods, it should be done from the beginning of a new financial year with proper disclosure in financial statements and tax audit report. Frequent changes attract scrutiny.

Q5: What if I discover errors in previous year’s books after filing tax audit?

If the error is significant and affects tax liability:

- File revised return if still within time limit (before end of assessment year or completion of assessment)

- If time limit expired, voluntary disclosure under Section 270A may reduce penalties

- Document the discovery and correction process

- Inform your auditor for current year’s report

Q6: Do I need to maintain separate books for GST and Income Tax?

No. Maintain one set of books that serves both purposes. The same sales register, purchase register, and ledgers should be used for both GST and Income Tax. This prevents mismatches and reduces compliance burden. Just ensure monthly reconciliation to keep them perfectly aligned.

Q7: What if my accountant maintains books but I don’t understand them?

This is dangerous. As a founder, you must understand your basic financials:

- Monthly revenue and expenses

- Profit/loss

- Cash flow

- Outstanding debtors and creditors

- Major expense categories

Request a monthly management report in simple language from your accountant. If they can’t explain it simply, consider changing accountants.

Q8: Can I backdate entries to “fix” mistakes?

Technically no, and it’s risky. Accounting software with audit trails will flag backdated entries. Instead:

- Make correcting entries in the current period with proper narration

- Use journal entries to adjust for previous period errors

- Maintain documentation explaining the correction

- Inform your auditor about material corrections

Q9: What’s the difference between Tax Audit under 44AB and Statutory Audit?

Tax Audit (Section 44AB):

- For Income Tax compliance

- Required if business turnover > ₹1 crore (or > ₹10 crore for cash receipts < 5%)

- Professionals > ₹50 lakh

- Focuses on tax compliance and correctness of accounts

- Form 3CD and 3CA/3CB filed

Statutory Audit:

- For Companies Act/LLP Act compliance

- Required for all private limited companies and LLPs (with some exemptions)

- Focuses on true and fair view of financial statements

- Audit report in prescribed format filed with ROC

Many businesses need both.

Q10: How often should I review my books – monthly, quarterly, or yearly?

Best practice:

- Daily: Basic recording (sales, purchases, expenses)

- Weekly: Bank reconciliation, payment tracking

- Monthly: Complete reconciliation, financial review, closure

- Quarterly: Detailed management review, tax planning, projections

- Yearly: Audit, finalization, strategic review

Monthly review is the minimum for any business serious about compliance.

Q11: What if my vendor doesn’t provide proper invoices?

You have limited options:

- Refuse to do business without proper invoice

- If unavoidable (small vendors), maintain detailed records: vendor name, address, payment proof, goods/service description, GST if registered

- Accept you may not get ITC on such purchases

- For regular vendors, make proper invoicing a contractual requirement

Never create fake invoices or accept invoices without actual transaction.

Q12: Can I claim home office expenses if I work from home?

Yes, but with proper documentation:

- If you own the home: Claim proportionate:

- Depreciation on the area used for business

- Property tax, insurance

- Repairs and maintenance

- Utilities (proportionate)

- If rented: Claim proportionate rent with agreement

- Critical: Must have dedicated workspace, not just working from dining table

Proportion should be reasonable (typically 10-25% of home).

Q13: What should I do if I receive a notice about book maintenance?

Don’t ignore it. Respond within the timeline (usually 15-30 days):

- Understand what specific issue is raised

- Gather all relevant books and documents

- Prepare a detailed response showing books are maintained

- If books genuinely weren’t maintained, acknowledge and rectify immediately

- Engage a CA for representation if complex

Q14: Is cloud-based accounting safe? What about data security?

Reputable cloud accounting platforms (Zoho, QuickBooks, Tally on cloud) have:

- Bank-grade encryption

- Regular backups

- Disaster recovery

- Access controls

Actually safer than local computers which can crash, get stolen, or damaged. However:

- Choose established platforms

- Use strong passwords

- Enable two-factor authentication

- Download periodic backups

Q15: What’s the biggest bookkeeping mistake you see founders make?

Mixing personal and business finances. This creates:

- Impossible reconciliation

- Personal expenses claimed as business (disallowed in audit)

- Unclear business profitability

- Tax complications

- Loan application difficulties

Solution: Separate bank accounts, separate credit cards, separate everything. Pay yourself a salary or drawing, then spend from personal account.

Final Word:

Think of maintaining books not as a compliance burden, but as building your business’s financial nervous system. Good books tell you:

- Where you’re making money (and where you’re losing it)

- Where cash is stuck

- Which customers/products are profitable

- When to expand and when to cut costs

They’re not just for the tax auditor – they’re for you. Build the system once, maintain it monthly, and you’ll never fear audit season again.

Still have questions? Contact AdvoFin Consulting for consultation.

📧 Email: info@advofinconsulting.com

📞 Phone: +91-92116-76467

🌐 Website: www.advofinconsulting.com

Disclaimer: This blog is for educational purposes only and does not constitute professional tax advice. Consult a qualified professional for specific situations.