Strategic corporate tax changes focus on competitive rates and positioning India as a global financial hub. Here’s the complete breakdown:

MINIMUM ALTERNATE TAX (MAT) – RATE CUT & STRUCTURAL CHANGE

What is MAT?

Background:

- Companies showing high book profits but low taxable income triggered MAT

- Ensured minimum 15% tax on book profits

- Applicable to companies under old tax regime (Section 115JB)

Not applicable to:

- Companies under new regime (Section 115BAA/115BAB @ 22%/15%)

Key Changes Effective FY 2026-27

1. MAT Rate Reduced

| Parameter | Old Rate (FY 2025-26) | New Rate (FY 2026-27) | Savings |

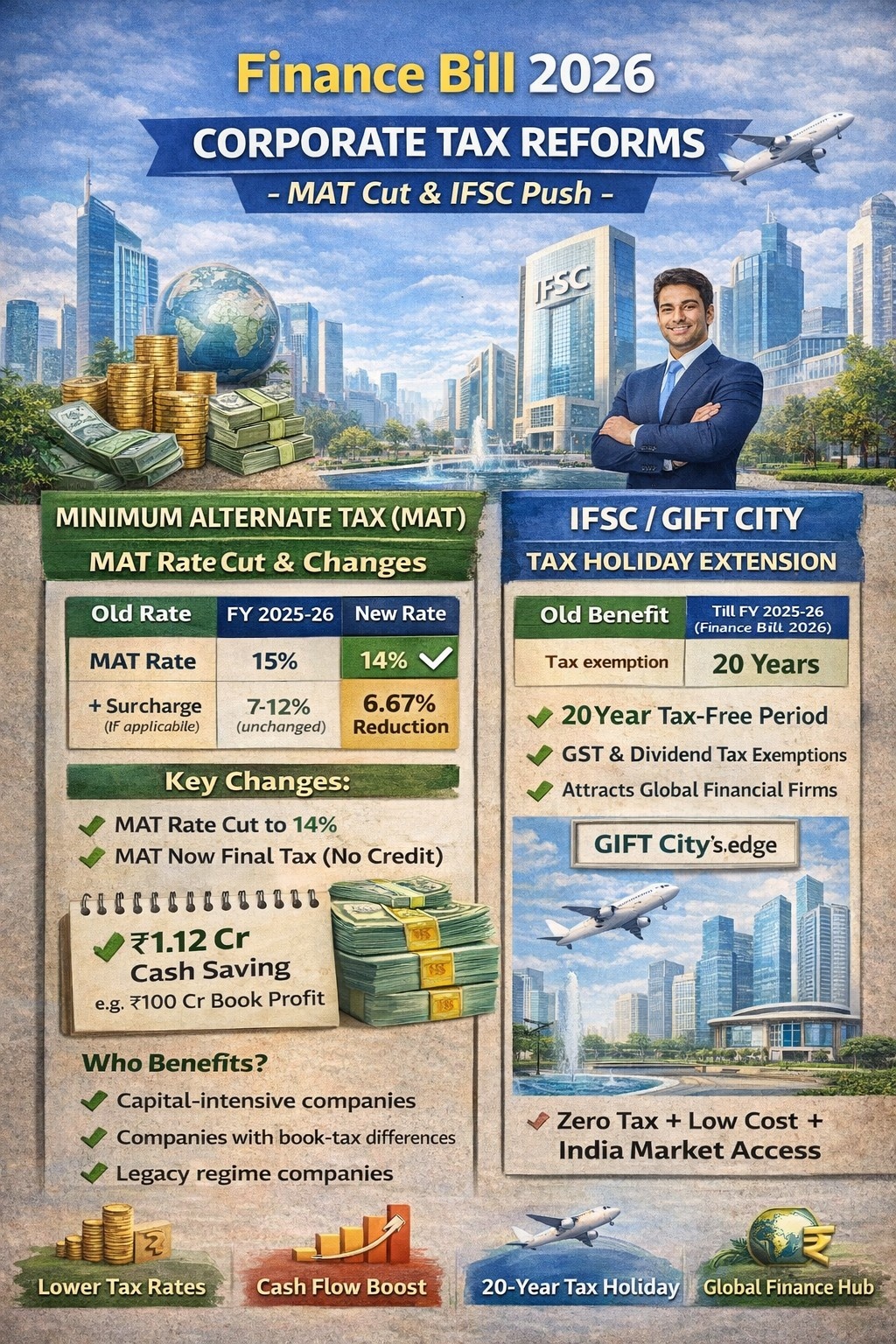

| MAT Rate | 15% | 14% ✅ | 6.67% reduction |

| + Surcharge (if applicable) | 7-12% | 7-12% (unchanged) | – |

| + Cess | 4% | 4% (unchanged) | – |

| Effective MAT | 15.6-17.5% | 14.6-16.2% | 1% absolute saving |

Example: MAT Calculation

Company: ABC Manufacturing Ltd (Old Regime)

Book Profit (as per Companies Act): ₹100 crore

Taxable Income (as per Income-tax Act): ₹40 crore

Normal corporate tax @ 30%: ₹12 crore

MAT Trigger: Book profit tax > Normal tax

MAT Calculation:

| Component | Old MAT (15%) | New MAT (14%) |

| Book Profit | ₹100 Cr | ₹100 Cr |

| MAT Rate | 15% | 14% |

| MAT Amount | ₹15 Cr | ₹14 Cr |

| Surcharge (assume 7%) | ₹1.05 Cr | ₹0.98 Cr |

| Cess @ 4% | ₹0.64 Cr | ₹0.59 Cr |

| Total Tax Payable | ₹16.69 Cr | ₹15.57 Cr |

| Savings | – | ₹1.12 Cr ✅ |

Impact: ₹1.12 crore cash saving for company

2. MAT Made FINAL TAX (No Credit Mechanism)

BIGGEST STRUCTURAL CHANGE

Old MAT Credit System (Till FY 2025-26):

Step 1: Company pays MAT in Year 1 (₹15 crore on ₹100 Cr book profit)

Step 2: Normal tax in Year 1 would’ve been ₹12 crore

Step 3: MAT Credit created: ₹15 Cr – ₹12 Cr = ₹3 Cr

Step 4: In Year 5, normal tax exceeds MAT

- Book profit: ₹120 Cr → MAT: ₹18 Cr

- Taxable income: ₹100 Cr → Normal tax: ₹30 Cr

- Normal tax > MAT, so pay ₹30 Cr

Step 5: Utilize MAT Credit of ₹3 Cr from Year 1

- Final tax: ₹30 Cr – ₹3 Cr = ₹27 Cr ✅

Benefit: MAT credit recovered over 15 years

New MAT System (From FY 2026-27):

Step 1: Company pays MAT in Year 1 (₹14 crore on ₹100 Cr book profit)

Step 2: Normal tax would’ve been ₹12 crore

Step 3: NO MAT Credit created

Step 4: In Year 5, when normal tax > MAT

- Pay full ₹30 Cr normal tax

- Cannot utilize any credit from past years

Result: MAT is now a final, non-refundable tax

Comparison Table: MAT Credit Impact

| Scenario | Old System | New System (From FY 26-27) |

| MAT paid in Year 1 | ₹15 Cr | ₹14 Cr |

| Normal tax (Year 1) | ₹12 Cr | ₹12 Cr |

| MAT Credit created | ₹3 Cr ✅ | NIL ❌ |

| Carry forward period | 15 years | Not applicable |

| Utilization in future years | Yes (when normal tax > MAT) | No ❌ |

| Effective cost | Timing difference only | Permanent cost |

What About Existing MAT Credits?

Partial Usability When Shifting Regimes

Scenario: Company has ₹10 crore MAT credit accumulated till FY 2025-26

Option 1: Stay in Old Regime

- Continue paying MAT @ 14% (reduced rate)

- Cannot create new MAT credits from FY 26-27 onwards

- Existing ₹10 Cr credit: Can utilize when normal tax > MAT (next 15 years)

Option 2: Shift to New Regime (22%/15%)

- Existing ₹10 Cr credit: Only partially usable (conditions apply)

- Usually capped or time-limited

- Check specific transition rules

Recommendation: Stay in old regime if large MAT credit balance exists

Who Benefits from MAT Rate Cut?

– Capital-intensive companies:

- High depreciation in books (lower taxable income)

- Heavy plant & machinery investments

- Examples: Manufacturing, infrastructure, power

– Companies with Book-Tax Differences:

- Unabsorbed losses (tax books) vs. profits (book accounts)

- Section 43B disallowances

- Provision-based expenses

– Companies preferring old regime:

- Want to claim deductions (Section 80IC, 80IE, etc.)

- Benefit from lower MAT @ 14% vs. new regime @ 22%

Who’s Unaffected?

❌ New regime companies (Section 115BAA/115BAB):

- Pay flat 22% (manufacturing) or 15% (new manufacturing)

- MAT doesn’t apply

- This change irrelevant

❌ Companies with normal tax > MAT:

- Already paying regular corporate tax

- MAT never triggered

- No benefit from rate reduction

Should You Stay in Old Regime or Shift to New?

Decision Matrix (Post Finance Bill 2026):

| Factor | Old Regime | New Regime |

| Tax Rate | 30% (+ surcharge + cess) | 22% (manufacturing) / 15% (new setup) |

| MAT | 14% (if triggered) | Not applicable |

| MAT Credit | Existing usable; new NOT created | N/A |

| Deductions | 80IC, 80IE, 10AA, etc. available | No deductions allowed |

| Depreciation | Higher rates (WDV method) | Lower rates |

| Best for | Capital-heavy, loss-making, SEZ units | Profit-making services/light manufacturing |

Example Decision:

Company A: ₹50 Cr book profit, ₹10 Cr taxable income (high depreciation)

- Old regime MAT: ₹7 Cr (14% of ₹50 Cr)

- New regime tax: ₹2.2 Cr (22% of ₹10 Cr)

- Winner: New regime ✅

Company B: ₹50 Cr book profit, ₹5 Cr taxable income, ₹8 Cr 80IC deduction available

- Old regime: MAT ₹7 Cr (deductions don’t reduce MAT)

- New regime: ₹1.1 Cr (22% of ₹5 Cr, no 80IC)

- Winner: New regime (unless 80IC benefit > ₹5.9 Cr)

Rule of thumb: Most profitable companies benefit from new regime; MAT benefits capital-heavy/loss-making companies

IFSC / GIFT CITY INCENTIVES – TAX HOLIDAY EXTENDED

What is IFSC?

International Financial Services Centre (IFSC):

- India’s first IFSC: GIFT City, Gandhinagar, Gujarat

- Special Economic Zone for financial services

- Competes with Singapore, Dubai, Hong Kong

Activities allowed:

- Banking, insurance, asset management

- Aircraft/ship leasing

- Fund management, pension funds

- Commodity derivatives, bullion trading

Tax Holiday Extension – Section 80LA

Previous Benefit (Till FY 2025-26):

- 100% tax exemption on profits for IFSC units

- Available for 10 consecutive years (out of 15 years)

- Conditions:

- Unit set up before 31 March 2024

- Engaged in specified financial services

Limitation: Short 10-year window discouraged long-term setup

Extended Benefit (From FY 2026-27):

Tax holiday extended to 20 years

| Parameter | Old Benefit | New Benefit (Finance Bill 2026) |

| Tax exemption | 100% | 100% (unchanged) |

| Duration | 10 years (in 15-year block) | 20 years |

| Eligible units | Set up before 31-3-2024 | Set up before 31-3-2030 (likely extension) |

| Sectors covered | Banking, fund management, aircraft leasing, etc. | Expanded list (data centres mentioned separately) |

Example: IFSC Tax Savings

Company: XYZ Fund Management (IFSC Unit, GIFT City)

Annual profit: ₹100 crore

Tax rate (if regular domestic unit): 22% (new regime) = ₹22 crore tax

Tax Savings Over 20 Years:

| Year | Profit | Tax (without IFSC) | Tax (with IFSC exemption) | Annual Savings |

| Year 1-20 | ₹100 Cr/year | ₹22 Cr | ₹0 | ₹22 Cr |

| Total (20 years) | ₹2,000 Cr | ₹440 Cr | ₹0 | ₹440 Cr |

NPV of savings (@ 10% discount): ~₹187 crore

Massive incentive for global financial firms

Additional IFSC Benefits (Beyond Income Tax)

- GST exemption on financial services within IFSC

- No STT on securities traded in IFSC exchanges

- No commodity transaction tax (CTT)

- Simplified KYC norms for foreign clients

- 100% FDI allowed via automatic route

- Dividend distribution tax exemption

- Capital gains exemption for Category III AIFs in IFSC

Data Centre Exemption – NEW (Finance Bill 2026)

Section 10(48C) – Specific to IFSC Data Centres

Benefit:

- Foreign companies setting up/using data centres in IFSC

- 100% exemption on income from data centre services

- Approved Indian data centres under notification

Objective:

- Attract global tech/financial firms

- Build world-class digital infrastructure in GIFT City

- Compete with Singapore, Ireland for data centre hubs

Example:

- Google Cloud sets up data centre in GIFT City

- Revenue from cloud services to foreign clients: Tax-free

- Revenue from domestic clients: Regular tax applies

Who Benefits from IFSC Tax Holiday Extension?

– Global banks:

- HSBC, Standard Chartered, DBS already in GIFT City

- 20-year tax holiday = sustainable India operations

– Asset management companies:

- Offshore funds managed from India

- Tax-free fund management fees

– Aircraft/ship leasing companies:

- Major leasing hubs (competes with Ireland, Singapore)

- GIFT City now offers 20-year tax certainty

– Insurance companies:

- Reinsurance operations

- Captive insurance for global corporations

– Fintech/data firms:

- New data centre exemption

- Digital financial services platform

Comparison: GIFT City vs. Singapore/Dubai

| Factor | GIFT City (India) | Singapore | Dubai (DIFC) |

| Corporate tax | 0% (20 years) ✅ | 17% (some exemptions) | 0% (50 years in DIFC) |

| Regulatory framework | IFSCA (single regulator) | MAS | DFSA |

| Talent pool | Large, English-speaking | Excellent | Good (expat-heavy) |

| Time zone | India (GMT+5:30) | Singapore (GMT+8) | Dubai (GMT+4) |

| Connectivity | Emerging | Excellent | Excellent |

| Cost of operations | Low ✅ | High | Medium-High |

| Ease of doing business | Improving | Excellent | Excellent |

GIFT City’s edge: Zero tax + low cost + India market access

Government’s Vision for GIFT City

Target: Top 5 global financial centres by 2030

Current status: 600+ units registered, ₹6+ lakh crore AUM

Key sectors: Banking (30%), fund management (25%), fintech (20%)

Employment: 75,000+ professionals (target: 1 lakh by 2028)

Recent developments:

- NSE IFSC launched (competes with SGX for derivatives)

- Bullion exchange operational (India’s gold price discovery)

- REITs/InvITs listing framework introduced

COMPARATIVE TAX ANALYSIS

Corporate Tax Rates – Quick Reference (FY 2026-27)

| Company Type | Tax Regime | Rate | MAT Applicable? | Effective Rate |

| Domestic (old regime) | Sec 115BA | 30% | Yes (14%) | 30-34.9% or 14.6-16.2% |

| Domestic (new – manufacturing) | Sec 115BAA | 22% | No | 25.17% (with SC+cess) |

| Domestic (new setup – manuf) | Sec 115BAB | 15% | No | 17.16% (with SC+cess) |

| IFSC unit (GIFT City) | Sec 80LA | 0% | No | 0% ✅ |

| Foreign company (royalty) | – | 10-20% | No | 10-21% |

| Foreign company (data centre) | Sec 10(48C) | 0% (IFSC) | No | 0% ✅ |

STRATEGIC IMPLICATIONS

For CFOs & Tax Planners:

MAT Changes:

✅ Reassess old vs. new regime choice (14% MAT now more competitive)

✅ Stop relying on MAT credit for future tax planning (no new credits)

✅ Existing MAT credit: Utilize before shifting regimes

✅ Capital expenditure planning: Higher depreciation benefits old regime (triggers MAT @ 14%)

Action: Run 5-year projection comparing:

- Old regime (30% or MAT 14%, whichever higher)

- New regime (22%/15% flat)

For Businesses Considering IFSC:

20-year tax holiday = compelling business case:

– Financial services firms: Set up fund management/treasury in GIFT City

– Global banks: Expand IFSC operations (wholesale banking, wealth management)

– Tech companies: Data centre opportunities (new exemption)

– Aircraft/ship leasing: Tax-free lease rentals from global clients

Cost-benefit example:

- Setup cost in GIFT City: ₹10 crore

- Annual profit: ₹50 crore

- Tax saving (20 years): ₹200+ crore (NPV ~₹85 crore @ 10%)

- ROI on IFSC setup: 850% over 20 years ✅

For Foreign Investors:

India now offers:

- Tax-free operations in IFSC (20 years)

- Market access to India’s $3.7 trillion economy

- Lower costs vs. Singapore/Hong Kong (30-40% savings)

- English language, rule of law, skilled talent

Key consideration: Regulatory comfort vs. tax savings trade-off

Running a manufacturing unit with heavy capex?

Planning to set up financial services operations?

Evaluating GIFT City vs. Singapore/Dubai?

Let’s analyze your optimal tax structure.